If you are choosing a startup bank in 2026, do not look for one “perfect” option. Look for the best fit for your stage, cash balance, payment needs, and fundraising plans. For most U.S. startups, the strongest choices fall into two groups: startup-focused platforms that move fast and automate finance work, and larger banks that offer deeper treasury, lending, and global support as you scale.

Quick answer

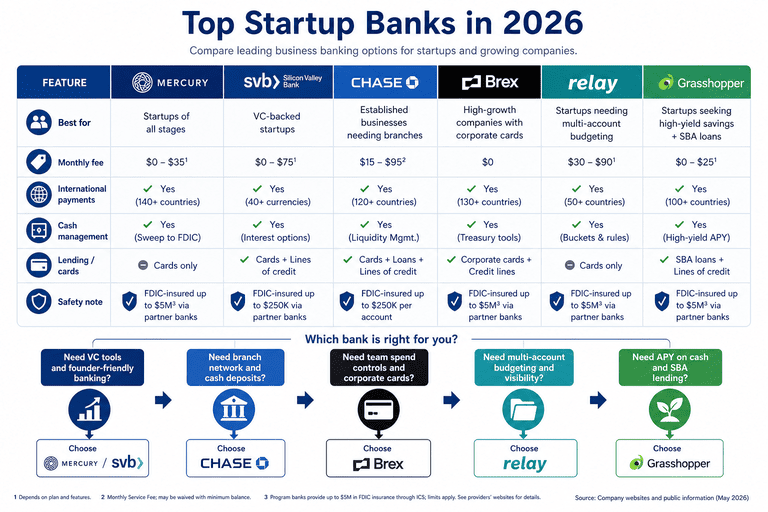

For most early teams, Mercury is the best all-around choice because it combines no monthly fees, fast setup, free ACH and domestic/international USD wires, team permissions, cards, and startup-friendly workflows. SVB is a top pick for venture-backed companies that want fundraising support and a stronger startup network. J.P. Morgan is one of the best options for startups that need global payments, treasury depth, and a bank that can support them from pre-seed through later stages. Relay, Grasshopper, Bluevine, and Brex are all strong depending on whether you care most about budgeting, yield, AP automation, or spend controls.

Comparison table

| Provider | Type | Best for | What stands out in 2026 | Main caution | Source |

|---|---|---|---|---|---|

| Mercury | Fintech platform with partner banks | Most software, SaaS, and early-stage startups | No monthly fees, free ACH, free domestic and international USD wires, team permissions, virtual and physical cards, startup perks, up to $5M FDIC insurance through partner banks and sweep networks | Not itself a bank; non-USD international wires have FX fees | Mercury |

| SVB | Chartered bank division of First Citizens | Venture-backed startups and founders actively fundraising | Startup-specific banking, founder network, investor connections, bill pay, money market options, digital banking, deep experience in tech and life sciences | Usually a better fit once your needs are more complex than basic checking | SVB |

| J.P. Morgan | Chartered global bank | Startups with international operations, treasury needs, or fast growth | Supports startups in 40+ countries, wires in nearly 70 currencies, treasury tools, cards, accounting sync, and no fees for up to three years on included services for eligible accounts | May feel heavier than a startup-only platform for a very small team | J.P. Morgan |

| Relay | Fintech platform | Founder-led teams that want clean cash buckets and simple approvals | Up to 20 checking accounts, employee cards, role-based access, ACH/wires/checks, strong bookkeeping sync, no hidden fees, up to $3M FDIC insurance available via Thread Bank | Better for operating discipline than for venture debt or startup fundraising support | Relay |

| Grasshopper Bank | Chartered digital bank | Startups that want yield plus startup-focused checking | Accelerator Checking and Savings, strong APY, startup eligibility, virtual cards, rewards debit, international payments, no monthly fees, enhanced FDIC coverage messaging | Less of a full venture ecosystem brand than SVB or J.P. Morgan | Grasshopper Bank |

| Bluevine | Fintech platform with partner bank and sweep network | Startups that want simple ops plus AP automation | Startup-focused checking, AP automation, physical and virtual debit cards, international wires, 3.0% APY on Premier, team permissions | Some best benefits sit behind specific plan tiers | Bluevine |

| Brex | Fintech finance platform with banking components | Teams that care most about spend control, cards, and finance workflow | Checking plus treasury and vault structure, up to $6M FDIC insurance in vault, many sub-accounts, strong spend tooling | Best when you want banking plus finance software, not just a plain bank account | Brex |

Infographic

Best picks by startup type

1. Best overall: Mercury

Mercury is the easiest recommendation for many startups because it removes friction. You can open accounts quickly, issue cards, set approval rules, send wires, and keep bookkeeping cleaner without paying monthly fees. It is especially strong for founders who want modern software and do not need a physical branch network.

2. Best for venture-backed startups: SVB

SVB is still one of the most useful names for startups that are raising capital or already backed by investors. Its edge is not just the account itself. It is the combination of startup bankers, investor connections, fundraising support, digital banking, and experience with innovation sectors like software, AI, fintech, and life sciences.

3. Best for global scale: J.P. Morgan

If your company is hiring internationally, paying vendors abroad, or moving toward a more serious treasury setup, J.P. Morgan is hard to ignore. Its startup program supports founders across stages, offers wires in nearly 70 currencies, and brings a much broader global banking stack than most startup-first platforms.

4. Best for cash organization: Relay

Relay is excellent for startups that want simple operating discipline. If you like the idea of separate accounts for payroll, tax, marketing, reserves, and vendor payments, Relay makes that easy. It is a very practical choice for bootstrapped companies, agencies, and small teams that want clean money management from day one.

5. Best for yield on operating cash: Grasshopper Bank

Grasshopper is one of the more interesting digital-bank options for startups in 2026 because it combines startup-focused checking with higher-yield deposit products. If you keep meaningful cash on balance sheet and want more return without giving up a startup-oriented experience, it deserves a serious look.

6. Best for AP workflows: Bluevine

Bluevine is a strong fit for founders who want one dashboard for checking, bills, cards, and payments. Its startup page focuses on AP automation, debit cards for teams, and international wires, which makes it useful for operating-heavy startups that want less manual finance work.

7. Best for spend management: Brex

Brex makes the most sense when company cards, approvals, policy controls, and finance workflow matter as much as the bank account. It is especially appealing to startups that already think of finance as a system, not just a checking account.

A practical founder guide to choosing the right bank

- Start with your real use case, not the brand name.

If you are bootstrapped, low fees and simplicity matter most. If you are funded, cash protection and treasury options matter more. That is also the core selection logic highlighted by NerdWallet. - Check whether the provider is a bank or a fintech platform.

That difference matters for risk, support structure, and how deposit insurance is delivered. Mercury, Bluevine, and some others clearly say banking services are provided through partner banks; SVB, Grasshopper, and J.P. Morgan are bank-led options. - Separate operating cash from reserve cash.

Your payroll and bills account should not also be your main reserve bucket. Many leading startup providers now offer checking plus higher-yield or sweep-style reserve options, which helps reduce operational risk and improves cash visibility. - Map your payment rails before you open the account.

List the things you will actually need in the next 12 months: ACH, domestic wires, international wires, cards for employees, approval flows, check payments, accounting sync, and perhaps FX. Choose the bank that matches that list, not the one with the best homepage copy. - Ask one question early: what happens when we scale?

A bank that feels great at pre-seed may become limiting at Series A if you need treasury tools, lending, investor intros, or multi-country support. This is where SVB and J.P. Morgan usually become more attractive.

Safety guide for founders

The safest setup is usually not “pick one famous name and forget it.” The safer approach is to understand how deposit protection works, verify the actual insured bank behind the product, and spread large balances when needed. The FDIC says deposit insurance covers at least $250,000 per depositor, per ownership category, per FDIC-insured bank. It also says coverage applies to deposits at FDIC-insured banks, not to every non-deposit investment product.

Here is the simple safety checklist:

- Verify the actual bank entity behind the account.

- Confirm how deposit insurance is structured.

- Keep runway cash separate from daily operating cash.

- Do not assume “fintech” means “bank.”

- Review sweep or vault structures if balances rise far above standard insurance limits.

- Recheck support quality, fraud controls, and approval workflows before wiring large sums.

My practical shortlist

If I had to make this simple for a founder in 2026, I would use this shortlist:

- Choose Mercury if you want the best default choice for a modern U.S. startup.

- Choose SVB if you are VC-backed or fundraising and want a startup network, not just a checking account.

- Choose J.P. Morgan if you need global reach, treasury depth, or a bank that can scale with a serious finance team. J.P. Morgan

- Choose Relay if you want clean budgeting and strong role-based controls.

- Choose Grasshopper if yield and startup-focused digital banking matter most.

- Choose Bluevine if AP automation and simple day-to-day operations are the priority.

- Choose Brex if cards, spend policies, and finance workflow are central to how your team operates.

FAQ

Where can i find the best bank for startups?

Start by comparing official product pages, not just review sites. Look at fees, insurance structure, payment types, approval controls, accounting integrations, and whether the provider is a bank or a platform using partner banks. Then match those facts to your stage and cash profile.

What are the best banks for early-stage startups?

For many early-stage teams, the strongest choices are Mercury, Relay, Bluevine, and Grasshopper because they are easier to set up and run than a traditional bank-heavy stack. If the company is already fundraising or expects investor introductions and more complex treasury needs, SVB becomes much more compelling.

What are the best banking options for startups?

The best option depends on what you optimize for. For simplicity, choose Mercury. For venture-backed growth, choose SVB. For global treasury and scale, choose J.P. Morgan. For AP and operating workflow, choose Bluevine or Brex. For structured cash buckets, choose Relay. For yield plus startup banking, choose Grasshopper.

What is the safest bank for pre-seed startups?

The safest choice is usually the one with the clearest insurance structure, the fewest operational surprises, and controls your team will actually use correctly. For small balances, a simple bank or startup platform with strong permissions can be enough. As balances grow, safety improves when you understand FDIC limits, verify partner-bank disclosures, and spread funds intelligently rather than relying on one account by habit.

Final takeaway

The best startup bank in 2026 is not the same for every founder. Mercury is the best default choice for many startups. SVB is one of the best choices for venture-backed companies. J.P. Morgan is the strongest step-up option for international scale and treasury complexity. Relay, Grasshopper, Bluevine, and Brex each win in a clear use case. If you choose based on your actual workflows, insurance structure, and next-stage needs, you are much more likely to get banking right the first time.