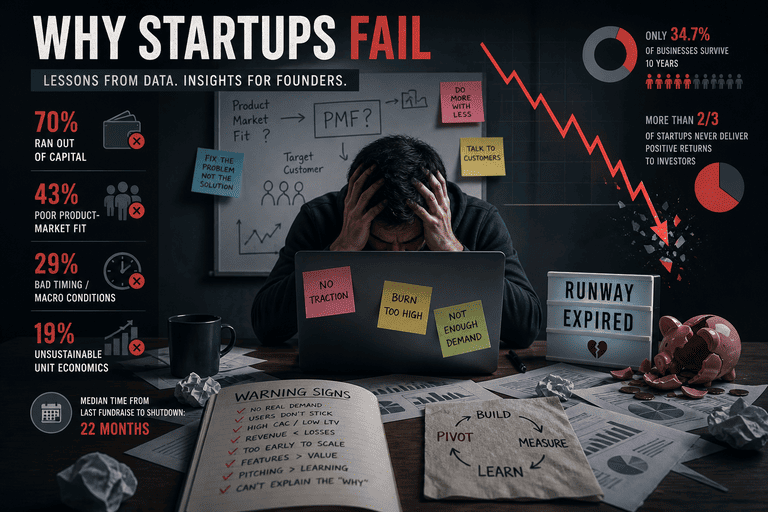

Short answer: most new startups do not begin with a classic large-company corporate card. They usually start in one of two lanes:

- a small-business credit card from a bank if the founder has solid personal credit and wants a simple, low-fee setup, or

- a startup-focused spend platform like Ramp or Brex if the company is funded, has meaningful cash in the bank, and wants higher limits, tighter controls, and less reliance on the founder’s personal credit. Stripe’s guidance is a useful reality check here: true corporate cards are typically aimed at businesses with much higher revenue, while smaller companies usually start with small-business credit cards.

This article is US-focused, because approval rules, underwriting, and card products vary a lot by country. If you are outside the US, the decision framework still applies, but the exact card names may be different.

Quick infographic

CopySTARTUP CARD PATH

New startup

│

├── Bootstrapped / little revenue / founder has good personal credit

│ └── Start with a simple bank small-business card

│ Examples: Chase Ink, Amex Blue Business cards

│

└── Funded / strong cash balance / wants no-PG style options and controls

└── Start with a startup-focused spend platform

Examples: Ramp, Brex

What matters most early:

low friction → clean expense tracking → employee cards → accounting sync → room to scale

This is the pattern most founders end up following because it matches how issuers actually underwrite risk: banks still lean heavily on the founder’s personal credit, while startup spend platforms often look at business cash, revenue, or funding.

Visual references

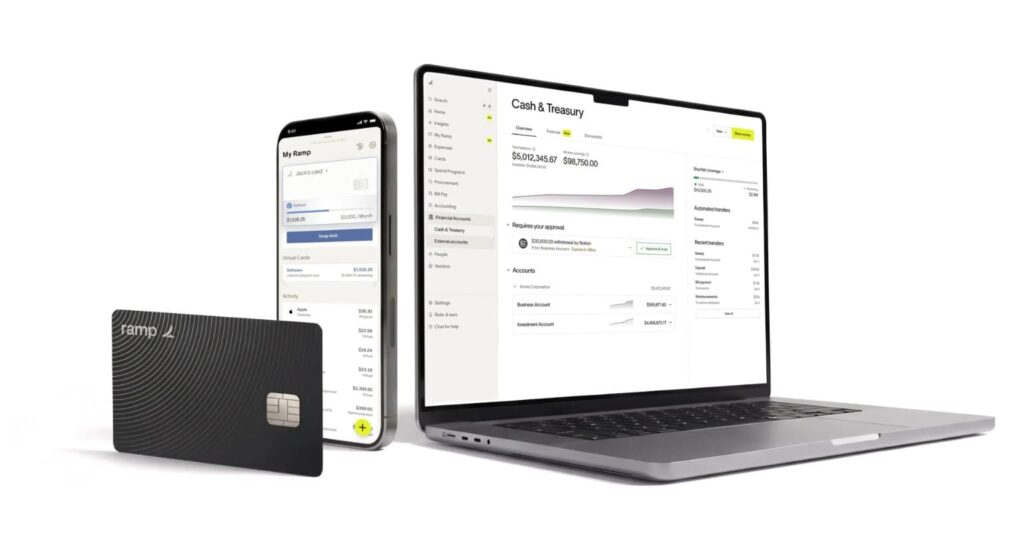

Ramp positions itself as a startup finance stack with cards, expense controls, bill pay, and partner perks.

Brex presents itself as an all-in-one stack for venture-backed startups with business-based underwriting and spend controls.

Chase’s no-annual-fee Ink cards are common starting points for straightforward cash-back setups. Chase

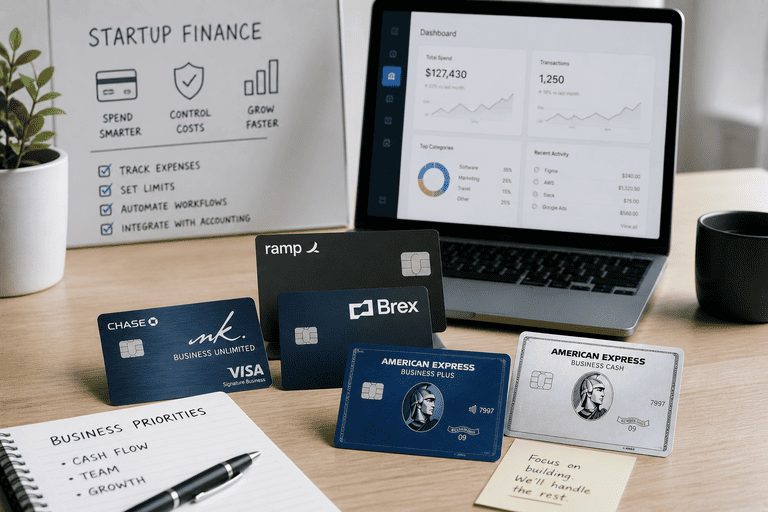

What startups usually choose first

In practice, bootstrapped startups often start with a simple bank business card that has no annual fee, basic employee cards, and easy cash-back rewards. The reason is simple: they want clean bookkeeping, a separate business spend line, and a tool that is easy to explain to an accountant. That is why cards like Chase Ink Business Unlimited and the entry-level American Express business cards are such common first picks.

Funded startups often move earlier to platforms like Ramp or Brex because these products are designed around business cash, spend controls, virtual cards, and accounting workflows. That matters when multiple employees need cards, approval flows, or department-level budgets.

If you need a corporate card for startups, the usual shortlist is Ramp or Brex, not a traditional bank travel card. Both focus on spend management, virtual cards, and approval logic based more on business health than on the founder’s personal score alone.

If you mainly want a company card for startups, most founders begin with a no-annual-fee bank card first and only upgrade later when expense controls, approvals, and multi-user workflows become painful. That path is usually cheaper and simpler in the first 6 to 12 months.

Ramp vs Brex vs bank cards: the practical difference

A bank card is usually best when your main goals are to separate business and personal spending, build credit history, and earn simple rewards. The trade-off is that approval often depends heavily on the founder’s personal credit and may include a personal guarantee. SBA guidance also notes that personal credit is commonly used in business card decisions.

Ramp and Brex are usually better when your startup already has decent cash reserves, raised capital, or needs team-wide controls. Ramp says startups without revenue should look for providers that assess cash on hand, bank balances, or investor backing, while Brex explains that its startup card model looks at business cash balance, revenue, and cash flow instead of requiring a standard personal credit check.

Stripe’s guide is especially useful because it cuts through the marketing: smaller businesses usually start with small-business credit cards, while larger firms with much higher revenue are the ones that typically qualify for classic corporate cards. That is why so many early founders start with a bank card first, unless they clearly fit the startup-fintech path.

top business cards for startups

| Card | Best fit | Why founders start here | Key official details | Main watch-out |

|---|---|---|---|---|

| Chase Ink Business Unlimited | Bootstrapped founders who want simple cash back | Easy-to-understand rewards, no annual fee, employee cards | Unlimited 1.5% cash back, employee cards at no additional cost, no annual fee shown on Chase business card pages | Traditional bank underwriting may lean on founder credit |

| American Express Blue Business Plus | Startups that want points with no annual fee | Strong simple rewards on general spend | 2X points on the first $50,000 in eligible purchases each year, then 1X; $0 annual fee | Amex acceptance is good but not universal everywhere |

| American Express Blue Business Cash | Teams that prefer cash back over points | Very simple rewards structure | 2% cash back on the first $50,000 in eligible purchases each year, then 1%; $0 annual fee | Best value depends on your spend profile |

| Ramp | Funded or cash-strong startups that need controls | Expense automation, virtual cards, policies, finance workflows | Apply in 2 minutes; review can take 1–2 business days; AI-powered rules; $350K+ in perks | Better fit once you have real operating spend and team usage |

| Brex | Venture-backed or scaling startups | Business-based underwriting, high limits, controls, startup ecosystem | No personal guarantee required; credit based on revenue or dollars raised; unlimited virtual and physical cards | Not aimed at tiny local businesses or solo operators |

| American Express Business Gold | Startups with concentrated category spend | Better for teams spending heavily in a few categories | 4X points on top 2 eligible categories each month; $375 annual fee | Usually not the first card unless spend is already high enough to justify the fee |

How to choose in 10 minutes

- If you are pre-revenue and bootstrapped, start with a simple bank business card. You are optimizing for approval odds, low fees, and basic bookkeeping, not a full finance stack.

- If you raised money or keep meaningful cash in the bank, compare Ramp and Brex first. Their model is built for startups that need cards for multiple people and better spend controls from day one.

- If your spend is broad and boring, prefer simple rewards. A flat-rate card is usually better than a complicated rewards chart when your purchases are spread across software, contractors, cloud bills, travel, and even niche items like fashion design ai prompts.

- If you plan to carry balances, care about APR and fees more than perks. SBA explicitly recommends reviewing intro APR, fees, and credit-reporting behavior before focusing on rewards.

- If you want to build business credit cleanly, check reporting behavior. SBA says this matters more than many founders think, because the right reporting setup can help establish the company’s credit profile while limiting personal-credit spillover.

The best professional guides worth reading

The most useful “how to think about this” guide is Stripe’s corporate card guide because it gives a clean rule: larger firms typically fit corporate cards, while smaller companies should usually begin with small-business credit cards. That helps founders avoid applying for the wrong product type too early.

The most useful “how to choose as a startup” guide is Ramp’s startup business credit card guide. It gives a practical checklist: build business credit, review fees, align rewards with actual burn, look for spend controls, and make sure accounting and tax workflows are covered.

For foundational basics, SBA’s establish business credit page and SBA’s business card evaluation guide are excellent. They are less flashy than issuer pages, but they are strong on the fundamentals: personal vs business credit, reporting, fees, APR, and business identity setup.

For founders who want a straightforward, human explanation of why a business card matters early, Clearco’s founder guide is one of the more practical reads. It explains the everyday reasons clearly: separate finances, build business credit, and get working capital without mixing everything into personal cards.

What I would recommend by startup type

Bootstrapped SaaS, agency, or solo founder with good personal credit: start with Chase Ink Business Unlimited or one of the Amex no-fee business cards. That is the cleanest and least complicated route.

Seed-funded startup with multiple employees: start by comparing Ramp and Brex first, because expense controls, virtual cards, and policy automation become much more valuable once spend is spread across a team.

Startup with high, concentrated ad or travel spend: consider whether a premium rewards card is worth it, but only if the annual fee is clearly justified by your actual spending pattern. The Amex Business Gold family page is a good example of a card that can make sense later, not necessarily first.

Very new founder with weak personal credit and limited cash: do not over-optimize for perks. First build the company’s credit base, separate finances properly, and choose the path with the best approval odds. SBA explicitly recommends focusing on business credit foundations early.

FAQ

Which business credit card is best for startups

For most bootstrapped founders, the best first move is a simple no-annual-fee bank card with clear rewards and easy bookkeeping. In today’s market, that usually means a Chase Ink card or an entry-level Amex business card. If the startup is funded and needs team-wide controls, Ramp or Brex may be the better first move.

What cards approve new startups fast

The fastest path is usually either a simple bank business card when the founder already has strong personal credit, or a startup spend platform that looks at business cash and funding instead of only personal score. Ramp says applications can be completed quickly and reviewed in 1–2 business days, while Brex emphasizes approval based on business cash balance, revenue, and cash flow.

Which corporate cards are designed for startups?

The clearest startup-focused examples in this set are Ramp and Brex. Both are built around business spend controls, virtual cards, approvals, and startup-style underwriting rather than only traditional personal-credit logic.

Which business cards reward startups

For simple everyday rewards, Chase Ink Business Unlimited and the no-fee Amex business cards are practical starting points. For companies that value platform perks and finance tooling more than classic points programs, Brex and Ramp can be more useful than a standard rewards card.

Do founders usually need a personal guarantee at the start?

Often yes with traditional bank cards, because many issuers still evaluate the founder’s personal credit when making the approval decision. Startup-focused products can reduce that dependence, but they usually want stronger business cash or funding evidence instead.

Is it smarter to optimize for rewards or controls first?

Most early startups should optimize for simplicity, approval odds, and clean bookkeeping first. Rewards matter, but only after the card clearly fits the company’s real spending pattern and operational needs.

Final takeaway

Most startups start with a simple business credit card first, not a heavyweight corporate product. If the company is small and founder-led, a no-fee bank card is usually the most practical first step. If the company is funded, has cash, and needs multi-user controls from the start, Ramp or Brex often make more sense. That is the clearest real-world answer to the question of what card startups usually start with.